Source: Michael Ballanger for Streetwise Reports 11/25/2019

Sector expert Michael Ballanger interprets year-end investment tactics by looking back at a childhood encounter.

“Gold is money; everything else is credit.” —J.P. Morgan

My first faithful dog Fido (circa 1963) and I used to play a game years ago before his eyes and hips started to go a tad “wonky,” and in that respect, we were and are quite similar. They say that dogs tend take on the appearance of their owners (or vice versa), so I guess that goes for the aging process as well. Anyway, we used to live in a neighborhood in the GTA that was once considered “working class:” That is to say, the wartime houses all looked the same (dull); were quite modest (small); and all were affordable (cheap).

However, the yards were actually disproportionate to the dwellings because my dad could flood a near-regulation-size hockey rink as long as the cops didn’t see him open up the local fire hydrant with that god-awful wrench the size of a baseball bat. In the winter, even on school nights, kids from around the neighborhood would be in the Stanley Cup finals until well after bedtime, as Dad strung up the ugliest set of lights in history to illuminate the playing surface.

As the winter wore on, the snow shoveled from the ice became the boards and after a number of mild spells where melting and refreezing occurred, those boards were the most unforgiving boards in hockey history. The nets were all made from 2x4s and fencing mesh so taut that if you really leaned into a shot, chances are it was coming right back at you twice as lethal as it was when it left your stick.

It was a mixed neighborhood with plenty of ethnic prejudice; being in an aircraft manufacturing town, it was filled with those awful immigrants from England and Ireland and Scotland that thought they actually belonged in Canada. As the legacy of the British Isles was carried across the Atlantic Ocean, the English looked down upon the Scots; the Scots and English looked down upon the Irish, and nobody but nobody tampered with anyone from Dublin. I know it wasn’t right but that was just the way it was—until you got on the ice, that is. Once on the ice, ethnicity disappeared and new battle lines were drawn and suddenly everyone wanted young Paddy from Dublin on their team and were willing to pay up. Suddenly and without reason, young Paddy was eating at your dinner table and was officially your “mate” (although Mother wondered for years after how any ten-year old boy could eat that many potatoes in one sitting).

Now, there was one kid named Harley who didn’t play hockey and as we all thought he was a little “strange” we tended to steer clear of him. Much larger than any of us, Harley took a different bus to school each morning and as we used to watch him duck to enter into the door of the bus, we would shudder to think of what would happen to us if he ever got mad (given that he probably was “mad”). One day, coming home from school, I came across an enormous black lunchbox lying unopened on the side of the road, and being of a curious nature (“nosy”), I opened it up and found a triple-decker peanut butter, jam and banana (!) sandwich staring up at me from under the Saran wrap that protected its infinite freshness. Now, peanut butter was good and a triple decker was better and a triple-decker peanut butter and jam was sublime, but throw in ripened banana slices and whoosh! Heaven. As Fido and I sat there devouring this tiny sliver of paradise (Fido kept smacking his canine lips to keep his mouth from sticking shut), around the corner appeared the visage of a large human being moving (stomping) toward us, apparently in ill humor. As he approached, a feeling of impending dread began to fill my psyche. When I finally realized who it was, I noticed a name, Harley, on the underside of the lunch box. which sent me scrambling to rewrap the half-eaten sandwich and stuff it under the apple and Mickey Mouse napkin.

Just as this leviathan of a boy reached down to grab me, the most remarkable thing occurred. Fido, having finally freed the peanut butter from the roof of his mouth, let out the most ungodly of growls and leapt in the air, his front paws landing squarely on Harley’s chest and, as if propelled by prehistoric instinct, fired poor Harley straight onto his back. Fearing for our lives the repercussions of assaulting this Neanderthal of a human, I ordered Fido to “Come!” Poised for flight, I watched in wonderment as each time Harley tried to get back on his feet, Fido would thump him back down. He never bit the kid but he never let him up either, and only when some adults came by and began to referee the altercation did Fido let up and trot back home with me, tongue wagging and supremely happy to have his teeth free from that hideous peanut butter. From that point on in my life, I called the Fido move “lockdown.” Fido the Wonder Dog was the master of “lockdown!“

What brought that little anecdote to mind was the recent action in the financial markets where the S&P 500 continues to shrug off weakening macro data, global trade and rising yields only to focus on a handful of momo stocks that are dominating the averages. Likewise, precious metals are bogged down in a range where rallies are constantly sold but also, due largely to physical demand, dips are being bought, particularly in silver.

The one word that comes to mind is, once again, “lockdown,” as it matters not the content of the headline event, with stock markets being at all-time highs; with gold and silver short positions now comfortably profitable coming off the early September highs; with year-end bonuses for the bullion bank traders firmly in the crosshairs. As we all have seen before, there is nothing more compelling than a seven-figure bonus at Hanukkah (or Christmas). Markets are in full lockdown and I find it hilarious to listen to CNBC as all of their “guest commentators” explain with great seriousness their “outlooks” and all of the minutia needed to explain why investors are choosing to ignore $80–100 billion a day (!) of REPO actions absolutely engorging the member banks with cash all for reasons about which we are supposed to “not worry.”

That said, the December silver contract is struggling within a downtrending triangle and absolutely must hold $16.75, the failure of which runs the risk of a quick plunge to the 200-dma (daily moving average) at $16.17. While I remain bullish, the upcoming week is going to be critical for near-term traders as we rapidly approach the First Notice Day, where gold open interest is coming down from its highest level in history. While silver is nowhere near as high, it is still in veritable lockdown unless it cracks $16.75.

Now, using Crimex #3 “Rule of Deception,” a breakdown of the $16.75 trendline could be the tape-painting exercise orchestrated by the bullion bank thieves to spook the funds and the amateur technicians into a high-volume dump, giving JPMorgan and brethren the opportunity to cover, after which they take it right back up. We shall see.

Shifting gears to stocks for a moment, I have been asked why, with the TVIX now down to under $7, I am not taking on a position. The reason is that I have become so disgusted with these constant interventions (PPT/REPO/tweets) that I feel like the mark in the rigged poker game. Anyone who can read and write can see how blatantly tilted the board has become. But I did pull up the TVIX chart and it actually looks like a very low-risk, high reward set-up. It’s a “buy.”

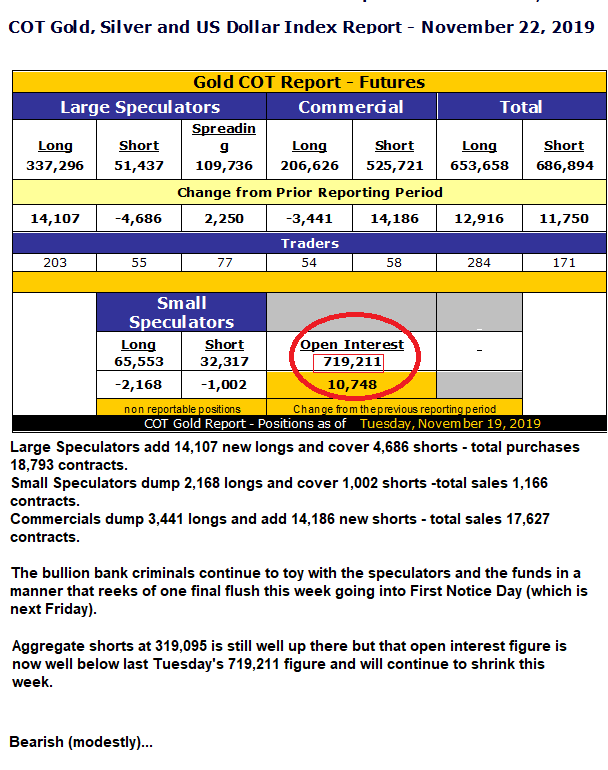

Last Tuesday’s COT carries few surprises, as it is consistent with today’s title. Large Specs want some? Commercials fill their orders. Large Specs need out? Commercials buy them. Wash. Rinse. Repeat. Total lockdown until Friday, then it all begins again with the Feb gold contract.

The TSX Venture Exchange has lost 4.88% year to date in a year that has seen the S&P rise 24%, with gold and silver up 14.23% and 9.4% respectively. Now, a great deal of that is the result of the bursting of the cannabis bubble in the summer, and since the wizards that run the TSX.V were all clamoring to get in on the action earlier this year and diversify away from the historical reliance on resources, the underperformance of the Canadian “gunslinger” exchange continues to act as a repellent to larger international capital flows that used to propel prices and funding activities over the past fifty years. I, for one, think that the TSX.V should stick to resources and let that cesspool Canadian Securities Exchange (the CSE) do the “flavor of the month” style of selection process that has served them so poorly here in 2019.

Regardless, my number one junior pick for 2019, Aftermath Silver Ltd. (AAG:TSX.V) (C$0.30), recommended in early July (just as the Georgian Bay boating season began) at CA$0.095/share, closed at CA$0.30 for the week, up 361.54% year to date, versus –4.88% for the TSX.V. By contrast, 2018’s darling (for a while, anyway) Aben Resources Ltd. (ABN:TSX.V; ABNAF:OTCQB), closed out last year in dismal form after I advised biting the bullet at CA$0.28. Despite a great deal of hype, it still sucked wind in 2019, closing out the week down another 46.67% year to date. This type of contrast in outcome is what keeps the large flows out of the Canadian junior markets.

Now, the list of companies mentioned in this publication includes good performers and poor performers, and while some were outright errors in timing, judgement and/or fortune (ABN, Stakeholder Gold Corp. [SRC:TSX.V], Canuc Resources Corp. [CDA:TSX.V]), others are in the tank but remain high on my list (Getchell Gold Corp. [GTCH:CSE], Western Uranium & Vanadium Corp. [WUC:CSE; WSTRF:OTCQX], Gem International Resources Inc. [GI:TSX.V)] and should be accumulated.

However, I have not wavered one iota in my enthusiasm for the management team and projects acquired by Mssrs. Williams and Rushton, and continue to accumulate more stock on each and every pullback since the last of the financings closed. The big news recently was the purchase by Eric Sprott of a 19.51% position in the company at $0.20 per share by way of a $2.98 million cash injection, which will essentially fund all activities in Chile for the foreseeable future.

Now, Eric Sprott is by no means infallible and his judgement is going to be rated by the two goddesses of mining (Mother Nature and Lady Luck) in the same way as are all mining projects. But one thing that can’t be denied is that Eric has a strong following and the eyes and ears of the institutional community. One look at what the Kirkland Lake Gold Inc. (KL:TSX; KL:NYSE) team did with Eric as chairman is proof positive that such involvement by such an accomplished investor, if nothing else, significantly improves our odds of succeeding. In this game, I will take any “edge” offered to me any day and all day. That, by the way, includes rabbits’ feet, St. Christopher medals, prayer and voodoo.

Also of note is that the recent financing announced by Getchell Gold Corp. (CA$0.10) looks to close next week oversubscribed (CA$1 million+), so the Fondaway acquisition is now a done deal and GTCH is the proud soon-to-be owner of a 1,069,000-ounce deposit. An old name from the past (Gem International) looks to close CA$500,000 next week as well, after coming out of purgatory, and was relisted on the TSX.V after a very painful (and embarrassing) eighteen months.

From the shape of the junior mining portion of the portfolio, had we not taken Great Bear Resources Ltd. (GBR:TSX.V; GTBDF:OTCQX) (CA$6.20) from $2.33 in January to $9.02 in September, and if we had not jumped on the Aftermath in July, there would now be bleeding eye sockets going into year-end, because the other names (Western Uranium and Stakeholder Gold) are either flat or lower for the year. As for the GGMA portfolio, it still remains ahead over 160% year to date (YTD), but will be pruned by mid-December to prepare for 2020.

Think of my trusty Fido the First and his classic lockdown move. Everything is in lockdown mode as portfolio managers strive to maintain their YTD profits. Mind you, it seems that everyone I talk to is mindful of this unearthly calm that has descended upon markets, so under the theory that markets do their utmost to hurt the majority of participants and reward the fewest possible, if there is a Black Swan event going into 2020, it will be a downside shock for stocks and a very pleasant upside surprise for the metals, where sentiment has once again shifted to despair.

Remember, rabbits’ feet, prayer, and voodoo. . .

Follow Michael Ballanger on Twitter @MiningJunkie.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Read what other experts are saying about:

- Aben Resources Ltd.

- Great Bear Resources Ltd.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver, Aben Resources, Western Uranium & Vanadium, Canuc Resources, Getchell, Stakeholder, Great Bear. My company has a financial relationship with the following companies referred to in this article: Aftermath, Getchell Gold and Western Uranium and Vanadium. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Aben Resources, Great Bear Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Aftermath. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver, Getchell, Canuc and Stakeholder, companies mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

( Companies Mentioned: ABN:TSX.V; ABNAF:OTCQB,

AAG:TSX.V,

CDA:TSX.V,

GI:TSX.V,

GTCH:CSE,

GBR:TSX.V; GTBDF:OTCQX,

SRC:TSX.V,

WUC:CSE; WSTRF:OTCQX,

)