Source: Michael Ballanger for Streetwise Reports 12/17/2019

Sector expert Michael Ballanger asserts that statements by American financial and political leaders are little more than market manipulations.

“Never trust anything a banker (broker) tells you.”—former billionaire (now millionaire)

Here is a news flash: I am sick to death of The Fed, unelected demigods that rarely, if ever, had to meet payroll. I am also completely disgusted with this unholy “Divine Right of Banks” to hold sway with politicians, gaining total control over the purchasing power of my savings (currency units) by way of an ordained edict giving them the right to manufacture any and all amounts of said currency units (debt) with nary a shred of governance.

I am further revolted by this all-encompassing blanket of regulatory malfeasance that condones and, in fact, encourages behaviors by C-suite officials, politicians and bankers in direct violation of securities laws. I refer to the practices of interventions (e.g., the Dec. 24, 2018, call by Treasury Secretary Steve Mnuchin for a meeting of the Working Group on Capital Markets”), manipulations (“tweets” designed to trigger software-generated reactions (President Trump, Elon Musk), and fraud (JP Morgan’s securities violations and RICO indictment). Lastly, this malevolent seepage of an innate sense of entitlement across the civilized world now threatens the foundation, support beams and roofs of the democratic system and along with it, free market capitalism, a phrase whose meaning Larry Kudlow would be wise to revisit.

In contract law, “due consideration” is that thing that allows a transaction to occur. It might be labor or a product or even advice, but essentially, it is a rules-based tenet that prevents theft. I cannot take something that is yours without you agreeing to that which I offer in trade. Last week, Fed chairman Jerome Powell explained the rules of the 2020 financial landscape by confirming to us all that “balance sheet normalization,” the implementation of which caused a20% meltdown in the S&P last year, is now, to borrow a phrase from Ebenezer Scrooge, “. . .an undigested bit of beef, a blot of mustard, a crumb of cheese, a fragment of an underdone potato.” In its place, we can now celebrate massive bloating of the Fed balance sheet, along with annual deficits to the order of $1.7 trillion.

In response, stocks began to slide, and precious metals began to rise, as the olfactory senses detected the imminent return of that elusive beast, inflation. It is said that inflation has been “muted” in the U.S. by way of cheap foreign goods (China) and subdued wage inflation. Mr. Powell told us, in his “prepared remarks,” that he and his co-conspirators are going to let the economy “run hot” for a while to allow Middle America to play “catch-up” in the disparity game of chance they are now playing with reckless abandon. The problem, my dear readers is that “inflation is like toothpaste; once it’s out you can hardly get it back in again” (Karl Otto Puhl).

What Chairman Powell meant to say is that Fed policies that have been engineering, promoting and cheerleading monetary asset inflation (all banker collateral, including stocks, bonds, and real estate) are now being back-burnered in favor of wage inflation (the income earned by the average Joe). News Flash #2: This policy “initiative” has no foundation in economic theory; it is a response to a societal trend whereby the disenfranchised segment of “The American Dream” is beginning to spiral out of control, with aberrant behaviors now more the norm than the isolated.

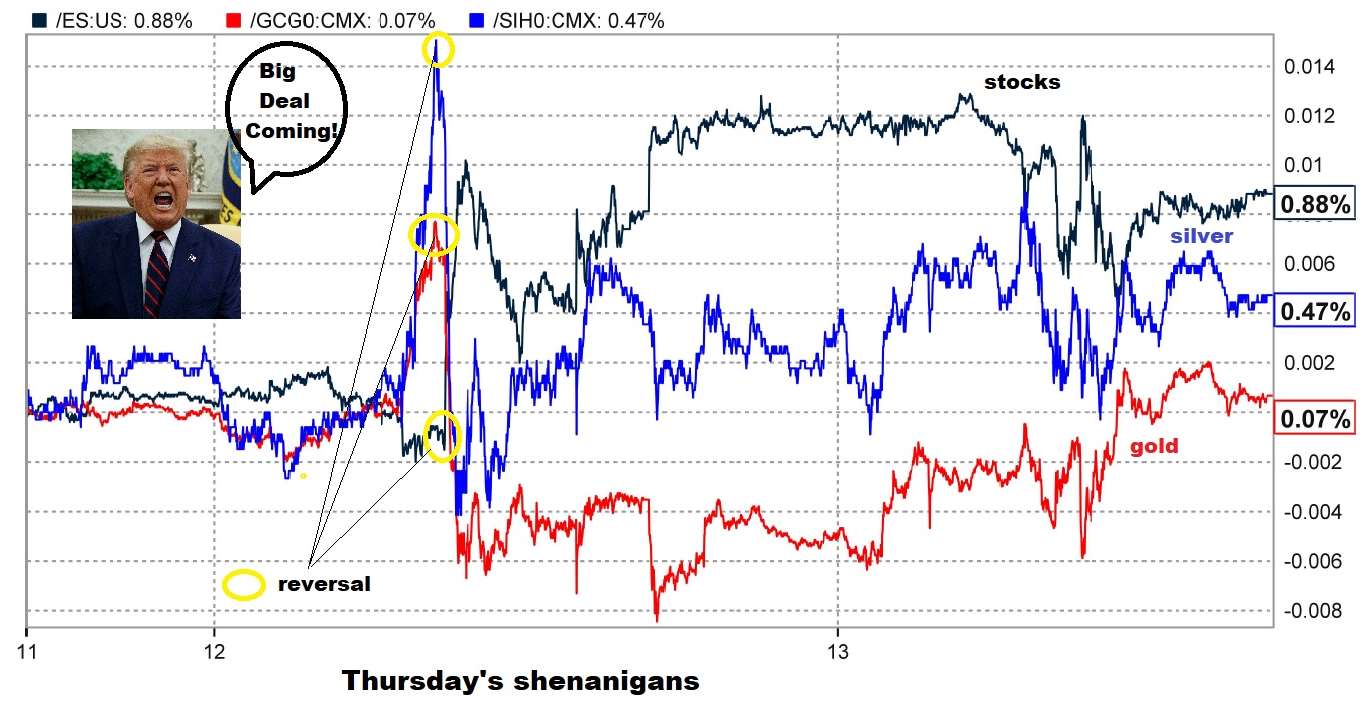

However, as minutes and seconds elapsed after the Powell Pronouncement, gold and silver began to escalate, with stock prices moving sharply lower. At this point, out of the blue and without explanation nor reason, Donald Trump fired off a tweet that was immediately absorbed by thousands upon thousands of pattern-recognition software word cloud analyzing “algobots,” stating emphatically that he is on the verge of signing a “BIG DEAL” with China that the markets “will love.”

As can be seen from the chart below, gold, silver and stocks all reversed and by the end of the day, the Dow had advanced over 200 points and all the beautiful gains in gold and silver had evaporated. All because a “China deal” tweet by Donald Trump, the fiftieth such market-moving utterance of 2019, spooked the algos into action, a manipulative trick well known and faithfully employed by the current Administration and its market co-managers.

When we decide to enter markets, we are told that manipulation is a violation of securities bylaws and an indictable offense. You can go to J-A-I-L for even attempting to influence markets by “spoofing” (stacking bids or offerings with phony orders never intended to be executed). Similarly, releasing false or misleading corporate or economic data is an action in violation of the rules as well. How the current POTUS can engage in such fraudulent behavior is astonishing; he has been calling for a China trade “deal” since 2018 and each and every time, the stock market rallied. Elon Musk was sanctioned for tweeting out that he was about to do Tesla deal at prices way above the current market, which also turned out to be a pile of horse manure designed to fry the shorts (which it did).

Now, “in the end,” you will say, “markets will revert to the norm and ignore the tweeting and spoofing and fraud,” because you believe these are “free markets.” News Flash #3: These are not, in any way, shape or form, free markets. These are the most compromised, corrupt entities in the world and until order is restored, they are as dangerous as a Cambodia mine field in the fog after a fifth of bourbon at midnight. And that restoration means jail time for violators—period.

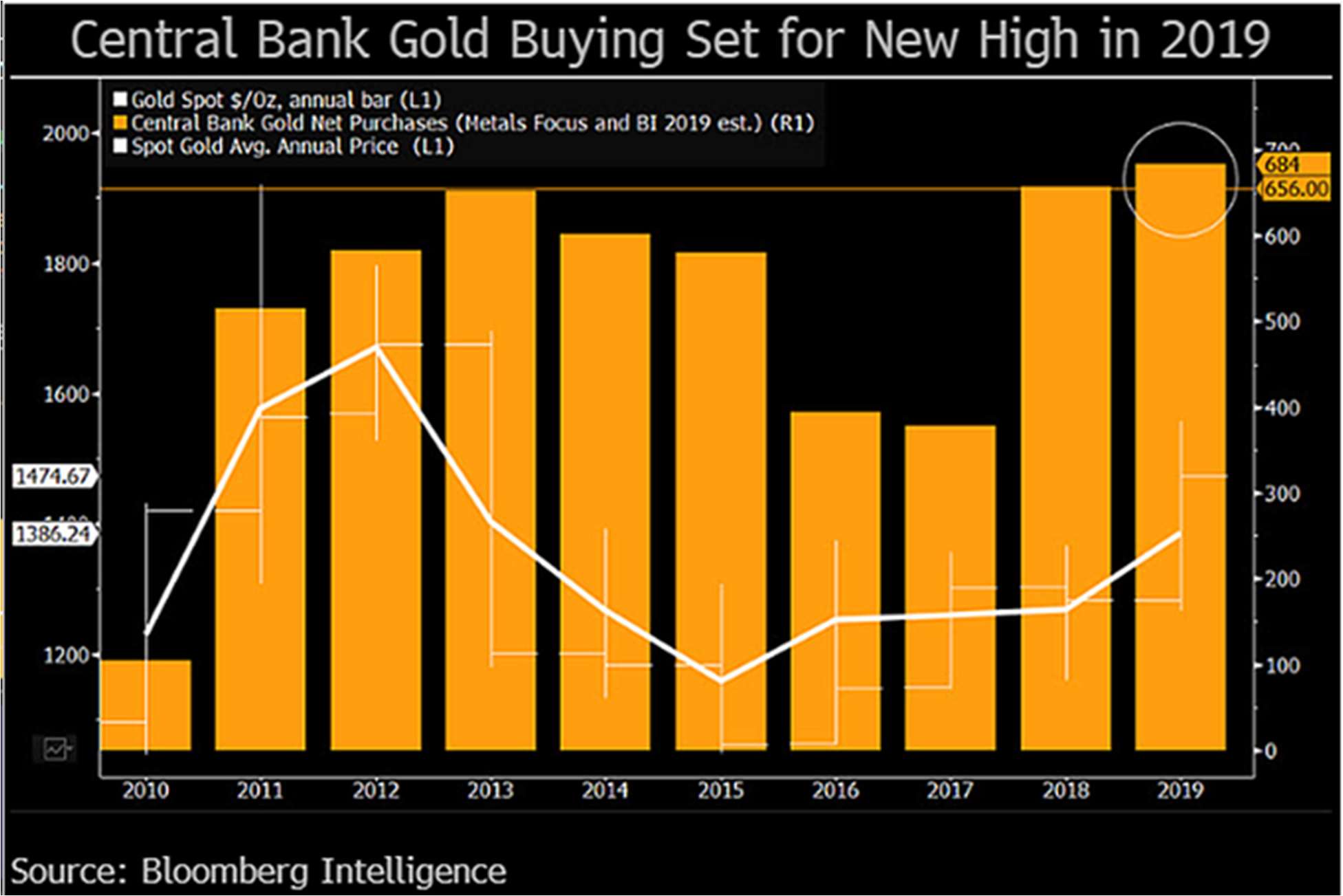

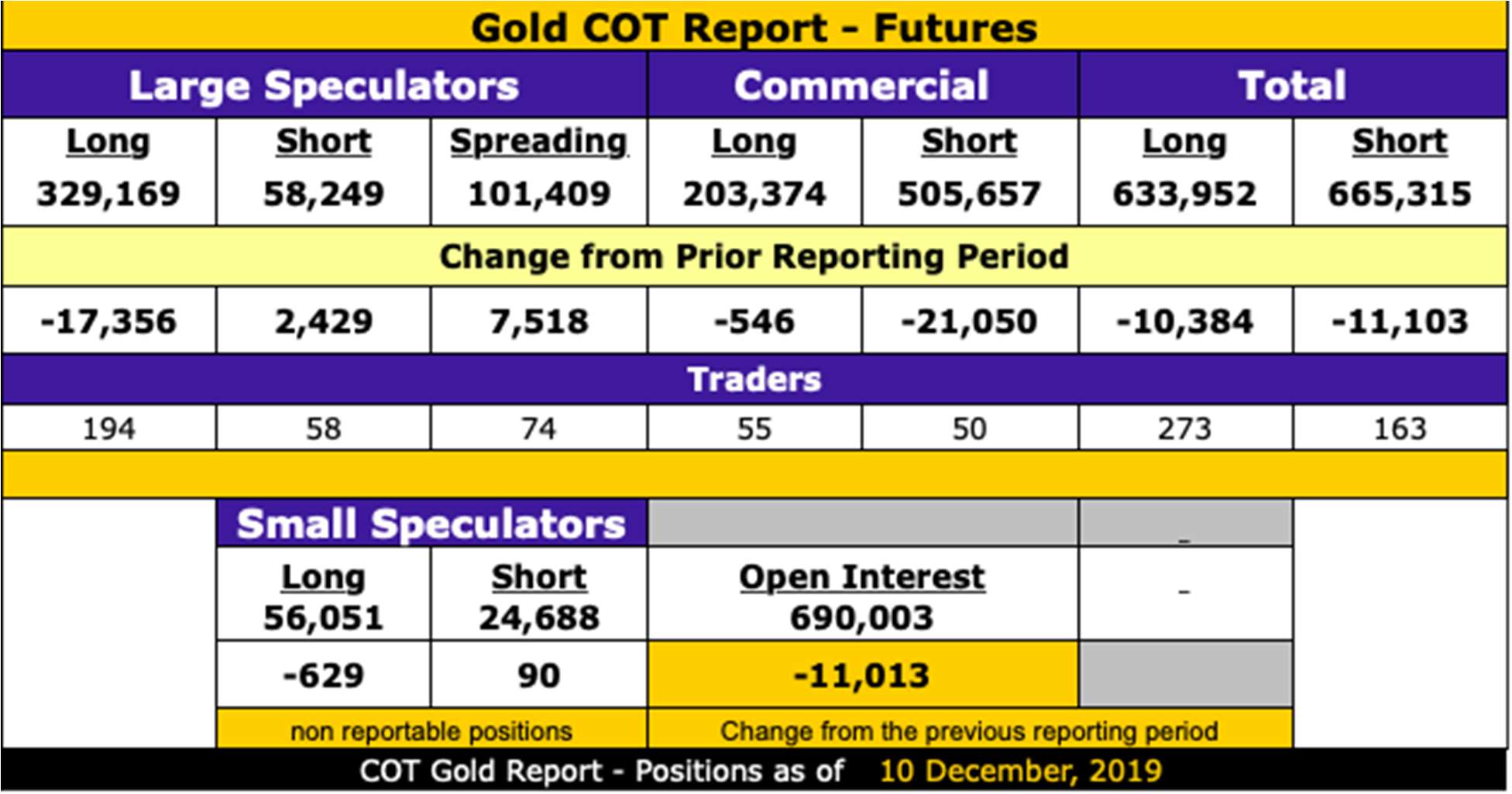

Nevertheless, for the week ended Dec. 13, the precious metals ended higher with the COT report, indicating good news for gold and great news for silver.

You can see that the weakness in early December triggered long liquidation by the Large Specs, accompanied by the usual reactionary short covering by the Commercials (bullion bank behemoths), along with the expected drawdown in open interest. While the strength this week will have prompted the reverse, the gold COT was positive and bodes well for a strong close for 2019.

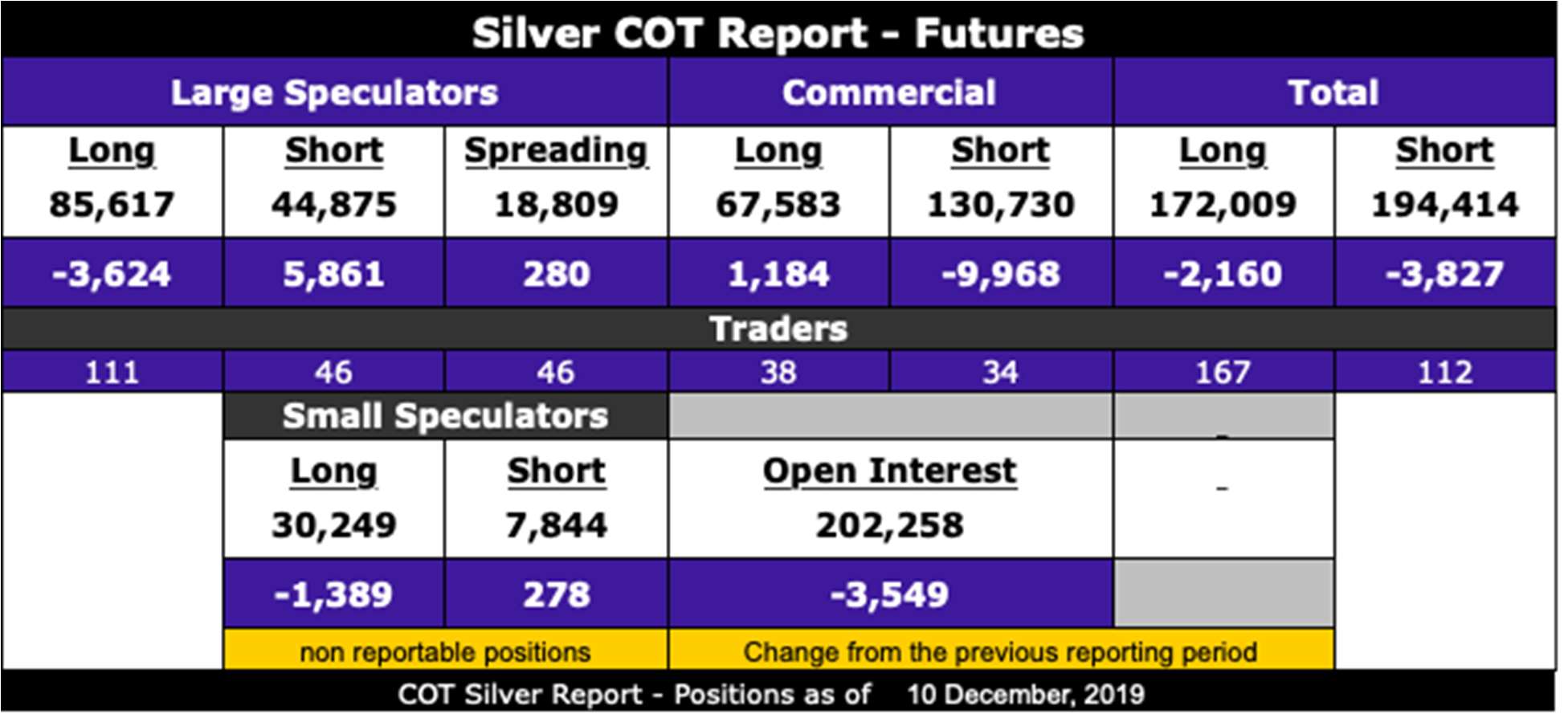

The silver COT was a shocker; the Commercials took full advantage of the big drop in early December, which came after First Notice Day (to my surprise and chagrin), and covered a massive 9,968 shorts, as well as adding 1,184 new longs representing 55,745,000 ounces of phony, never-to-be-delivered, “silver” with a fantasy-world notional value of US$947,665,000.

These bullion bank traders can whip around nearly a billion dollars’ worth of illusionary silver, materially impacting the livelihoods of mine laborers, pension fund managers, jewelers and solar energy dealers without as much as a whimper from the Securities and Exchange Commission, the U.S. Commodity Futures Trading Commission or the U.S. Department of Justice. However, it is what it is, and with silver ending the week higher, it remains my numero uno investment theme for 2020, as it was for the latter half of 2019.

In fact, it was silver options, futures and miners (as well as the Great Bear Resources Ltd. [GBR:TSX.V; GTBDF:OTCQX] trade, of course) that were responsible for the 273% advance in the GGMA portfolio, originally constructed in January 2019 and presented in the 2019 Forecast Issue. The silver market remains in a declining pennant formation, but with last week’s action, has clearly launched an assault on the downtrend line drawn off the Sept. 4 top (which I was lucky enough to have identified to the day back in late August).

I have identified the 200-day moving average (dma) at US$16.26 as the line-in-the-sand for short-term trading positions but certainly the actions on Thursday and Friday are encouraging.

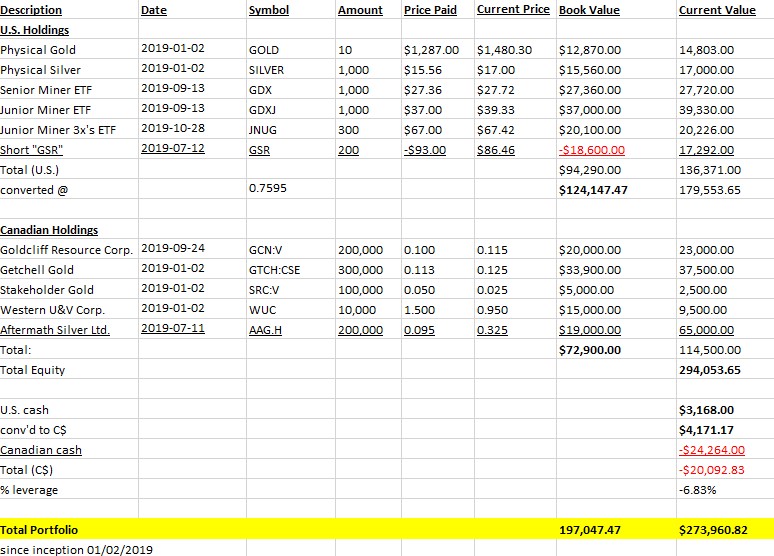

Turning to the GGMA portfolio, I am keeping the U.S. holdings intact going into the New Year but may take down the 3x-leveraged Junior Miner (JNUG), which is back into the black after going red almost immediately after acquisition. The original portfolio was purchased on Jan. 3, 2019, with CA$100,000, and with trades, additions and deletions, now resides at $294,053, with a CA$24,264 margin position, leaving total equity at CA$273,960. A return of 2.73 times original invested capital is both spectacular and unusual and was the product of some fortuitous positions taken in silver calls, Great Bear Resources (since sold) and Aftermath Silver Ltd. (AAG:TSX.V) (still holding and looking to add).

(As a bookkeeping note, the “Short GSR” position shows a red (negative) book value because it is a short sale andthe only way I could get it to jibe with the overall portfolio is to format it as such.)

As for the individual names, the Canadian dollar allocation is comprised of exclusively junior mining deals comprised of five exploration/development companies, all of which save one (Stakeholder Gold Corp. [SRC:TSX.V]) are sitting with established resources of either gold, silver or uranium. I am reviewing the SRC position closely but being a disappointment (verging on hallucinogenic flop), it is too small a holding to sell but providing zero impetus to buy. My top pick for 2019 was originally Great Bear, but has since been replaced with Aftermath Silver to close out the year.

Looking out to 2020, the forecast issue is in the oven, with a sneak peek available as to possible changes to the portfolio through my “2019 tax-Loss list,” where I have identified six companies floating in and around the 52-week low list being buffeted by wave after wave of tax-loss selling. (E-mail me at the address shown below on the contact card to receive a complimentary copy: Miningjunkie216@outlook.com.)

As much as I remain a staunch precious metals bull, I don’t think valuations here in late 2019 are as compelling as they were in August 2018 or April 2019. Those two entry points came off Daily Sentiment Index (DSI) readings of