Source: Maurice Jackson for Streetwise Reports 01/16/2020

In conversation with Maurice Jackson of Proven and Probable, the CEO elaborates on what could be a “company-making” event.

Maurice Jackson: Joining us for a conversation is David Cole of EMX Royalty Corp. (EMX:TSX.V; EMX:NYSE.American), the royalty generator. Pleasure to be speaking with you today to discuss a series of accretive transactions that EMX Royalty has consummated that continue to reward shareholders. Before we begin, Mr. Cole, for someone new to the value proposition, please introduce us to EMX Royalty and the opportunity the company presents to the market.

David Cole: We are a royalty generator. Royalties are phenomenal financial instruments. They are a slice off the top from metal production, so, if you own a 1% royalty on a project, 1% of the value of the metal that’s produced on that project goes to you. And the beauty of that is that it has embedded optionality. And that is exposure to additional discoveries, resource advancements, engineering advancements, etc., on that property to the benefit of the royalty holder at no cost to the royalty holder.

Therefore, it doesn’t matter how much capital is spent on the project, none of those bills come back to the royalty holder. We just get the 1% or 2% or 3% of the production that comes off that property. And also, of course, because these are commodities, we have commodity price optionality as well. As commodity prices move up or down, the payment structures for the value that represents can go up and down, and the long-term history is for commodity prices to rise.

The combination of commodity price optionality, discovery optionality and other aspects that add value to the royalty instrument makes royalties a really special thing. And the way we create them is through project generation, where we go out and we acquire prospective mineral rights, utilizing geological skill sets, add value, sell those for cash, shares, work commitments in the ground, and always a production royalty.

EMX Royalty has been successfully executing this business model for 16 years. We have 2.3 million acres of mineral right exposure and have approximately 70 royalties [around] the world.

Maurice Jackson: Truly is a wonderful value proposition. Let’s get everyone up to date on the company successes since our last interview, beginning in Turkey (Turkish assets), where EMX Royalty hosts seven projects dating back to 2003, when the company exercised its application of in-region geological knowledge as an early mover in its execution on its prospect generation business model.

Mr. Cole, take us to the Balya lead-zinc-silver mine, which was recently sold and where EMX holds an impressive 4% royalty on the property. What can you tell us about this transaction and its impact on EMX Royalty moving forward?

David Cole: The Balya royalty is an excellent example of exactly what we’re talking about. We acquired the Balya license from the Turkish government for $17,000 many years ago. We immediately executed geological modeling and delineation of prospective areas within that project. Sold it to a capable local Turkish company called Dedeman Madencilik for $100,000 in cash. We got all of our money back, plus more and a 4% production royalty. Dedeman went on to drill 59,000 meters of core and delineated multiple ore zones that are lead, zinc, silver rich on that property.

And then they started a test mine and had small tonnage. We’ve received some royalty payments from those. And now, they got bought out by their bigger neighbor, Esan Madencilik, [which] has a 5,000-ton per day mill. And that’s transformative to us, because now our ores, where we have that royalty, are going to go through the mill. It was a district consolidation [that] has substantial synergies. And we expect the production on this property to go up markedly over the course of the next two years—it will become a multimillion-dollar per year annual cash-flowing royalty at today’s metal prices.

Maurice Jackson: Moving northeast, let’s go to Serbia and discuss the recent developments at the giant Timok copper-gold deposit, where EMX holds a 0.5% royalty. Zijin Mining Group Co. Ltd. is advancing the Timok, and they are moving in an expeditious manner to get into production. Take us onsite, and share the progress that Zijin Mining is making on the Timok.

David Cole: You know, the Chinese are metal hungry. They just cannot own enough metal. They continue to be on a buying spree around the world. They paid over a billion dollars to buy this particular asset. They have signed a memorandum of understanding with the Serbian government, whereby they will invest US$474 million into the ground to advance the upper zone—the upper high-grade zone within that larger deposit that’s been found—into production very quickly.

We expect that to be in production in 2021. Based upon the feasibility study that was filed, our one-half of 1% royalty there [will] pay US$2.5 million per year in today’s metal prices. And we’re quite excited for that. That’s a nice augmentation cash flow.

But here’s where it becomes really interesting. And that is when they get into the huge lower zone. The lower zone is over a billion tons—a billion metric tons of mineralized rock that is defined within a compliant resource at 0.99% copper with a nice gold credit, so over 1% copper equivalent. And that’s going to be robustly economic in our opinion.

And the Chinese want the metal out of the ground. They’re moving forward very quickly. And when they get into the lower zone, our royalty payments are going to go up substantially. I believe this is a company-making event.

Maurice Jackson: Let’s take this conversation now to the United States. And let’s visit Nevada. Back in mid-December, EMX announced that they had acquired a 19.9% interest in the Rawhide Gold-Silver Mine. Can you walk us through how this might impact the future cash flow at EMX?

David Cole: One of the things that we do that makes us special is we also make strategic investments outside of the royalty sector. So, while our smart economic geologists and finance people are around the world identifying opportunities in the royalty space, if we see an investment opportunity that is so good that we cannot not do it, we will execute on that.

And our track record on our strategic investments is fantastic. It’s a 40% internal rate of return that’s compounded annually after tax on invested dollar over our 16-year history. [B]ecause of strategic investing gains [we] have as much money in the bank as we’ve raised in the history of the company, and no debt, in addition to the 2.3 million acres of mineral rights we have around the world.

So, that sets the stage, just so you understand how it is that we’ve made the strategic investment because it’s part of our business model, and when we’re sitting here with a large amount of cash and the capital markets are not robust right now in the mineral sector. Consequently, there’s a huge number of opportunities that are being shown to us.

People want us to invest money into their project, their company, etc. And so, we’re being shown a huge number of opportunities. And we have a team that’s comprised of an engineer, a metallurgist, geologists, finance guys, and we filter through those, and the vast majority of the things that we’re shown, they fail. But occasionally, one comes up. It’s like, holy smokes, this is very, very, very interesting.

I’ve personally been on site, toured the operation. It’s an active producing gold mine. They’re pouring ore almost every day. There’s a huge number of tons they have on the pad already and this will have, in our opinion, immediate cash flow. We’re expecting to have substantial cash flow from this. I’m not allowed to say the numbers until we put out a 43-101-compliant resource and production document that will define that. That’s in progress.

But we’re very happy with this investment. It meets all of our criteria and it’s going to give us additional cash flow in the near term. And we picked up to 20% of the Rawhide Mine for US$3.7 million. It was a great buy.

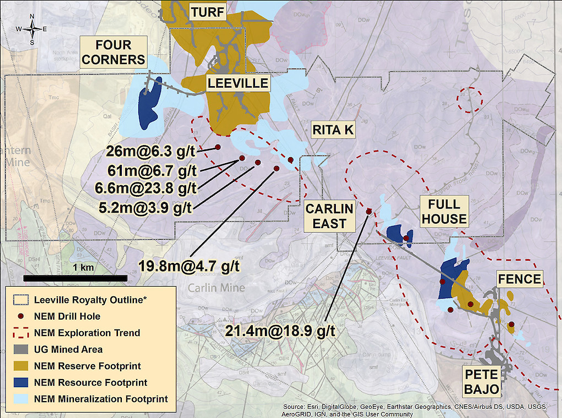

Maurice Jackson: Quite impressive. There are some interesting developments nearby as well, at the Leeville Complex. What can you share with us there?

David Cole: We’ve had the 1% royalty over Leeville—that’s a producing mine for a number of years now. It’s paid US$13 million to us already, in the time that we’ve owned that royalty. Newmont Goldcorp Corp. (NEM:NYSE) was the previous operator for the years that we’ve had that. Newmont’s also a shareholder in EMX. They own about 6% of our stock. We have good relationship with them. I worked for Newmont for 18 years before I left to found EMX Royalty Corp.

In fact, early in my career, I was involved in discovery of Leeville deposits. And Newmont and Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) formed a joint venture in Nevada where they pooled all their assets to take advantage of the synergies between the various infrastructure pieces that they had collectively in northern Nevada. And that joint venture company’s called Nevada Gold Mines. And Barrick is the operator of that.

When Barrick took over operation of all the assets including Leeville, as they managed Nevada Gold Mines, they came out with a new PowerPoint presentation where they were discussing the resource potential—they call it drill Indicated resource potential—on the Leeville property as well as other properties within the portfolio. And in that document—and that document’s publicly available on the Nevada Gold Mines website—they discuss Leeville in multiple places within their PowerPoint presentation.

It’s seems to be something that they’re very bullish on. And they delineate a large new zone that is drill indicated. And they show that the assays from drill holes [show] the stratigraphy with respect to where the gold mineralization is, and they talk about the total endowment of the whole region.

We can extrapolate, based upon the footprint of our royalty, relative to the entire Leeville complex. And we would estimate that what Barrick is suggesting is that there’s 10 million ounces in resource potential total, [which] would include the reserves, the resources, in addition to the drill Indicated resource potential. That’s the terminology that they use on our property.

And so, we’re extraordinarily happy about that. That’s why we originally acquired that 1% royalty—because we believe that there was excellent exploration development potential on that property. I will point out that Newmont completed a $300 million new shaft to enhance the underground infrastructure within the Leeville Complex a few years ago. It’s a property that these very large gold companies take extraordinarily seriously and we’re delighted to be a royalty holder on that.

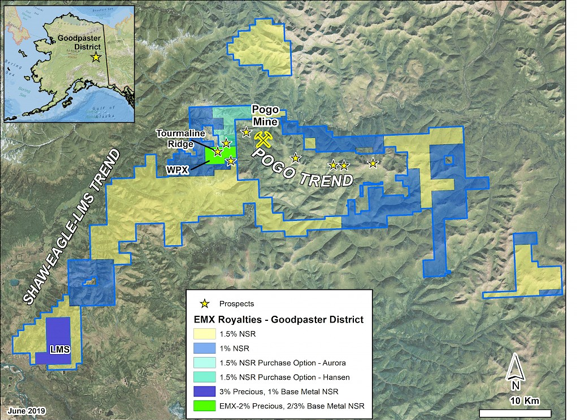

Maurice Jackson: Finally, let’s visit Alaska where EMX took a strategic position in Millrock Resources Inc. (MRO:TSX.V; MLRKF:OTCQB) to advance the formerly known Goodpaster project, now known as the 64 North Project. Do you have any updates to share with us?

David Cole: Well, that’s another example of us thinking laterally with respect to how to execute our business model. Greg Beischer, who is doing a great job of running Millrock, was low on capital and he had some excellent ideas about properties to acquire based upon their astute geological acumen. And he came to us, he says, “Dave, you know, I’ve got great ideas. I just need a few bucks.” I said, “Yeah, let’s do it.”

So, we invested money into his company at above-the-stock-price pricing. So, we got shares for doing that, in addition to royalties on the projects of which they acquired with that money. And that put us in a situation where we ended up with 233,000-acre percent, which is the number of acres of mineral rights times the percent royalty, and the royalty percentages vary block to block.

This transaction put us in a position where we’ve got a nice royalty over a growing gold district in Alaska. And then, subsequent to doing that deal, we’re delighted to be now strategic shareholders in Millrock. We think they do great work. They’ve executed a fantastic deal with an Australian company, where the Australian company’s going to come in and spend a bunch of money drilling. I’m not sure exactly how much it is. I think it’s $10 million per year for the next three years. It’s a salient amount of money.

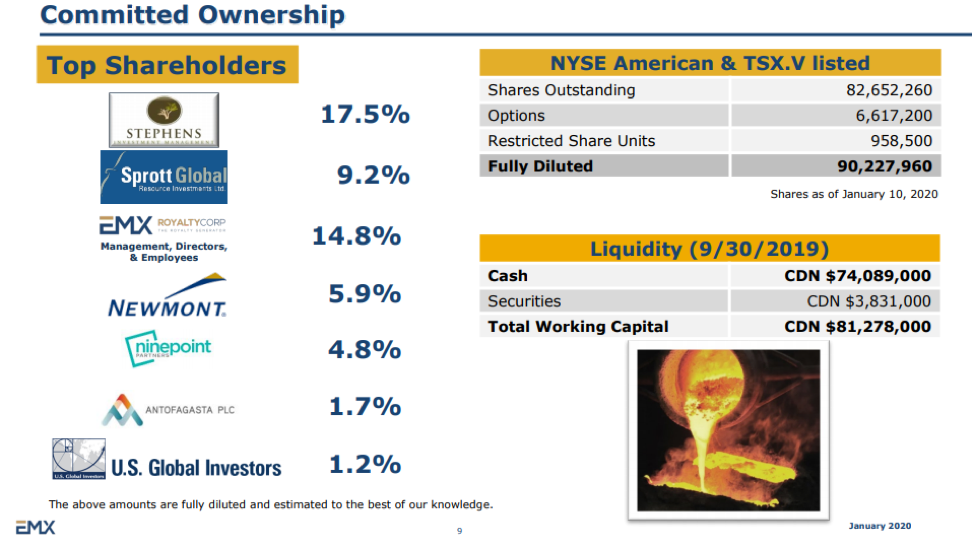

Maurice Jackson: Let’s look at some numbers. Mr. Cole, please provide us with the current capital structure for EMX Royalty.

David Cole: EMX Royalty has $81 million in working capital as of our last quarterly report—that’s in Canadian dollars. That would include $74 million in cash; no debt.

We have no debt on the books. And so, we’re in fantastic shape. That’s roughly all the money I’ve raised in the history of the company, in addition to our whole portfolio. And that’s definitive that the business model works, right? We’ve got all the money we’ve raised in the history of the company plus the whole mineral rights portfolio.

Maurice Jackson: I have noticed something as well, Mr. Cole. A lot of insider buying. Can you talk to us about who’s buying shares?

David Cole: Well, here we are with a substantial percentage of our market cap in cash, let alone all these great royalties and mineral assets we have around the world. And in my view, we’ve been substantially undervalued now for years, and that’s why I’ve been in the market buying. I’ve been buying for four years and all my trades are reported, of course. And I’m just delighted to continue to increase my percentage ownership in the company. I’m up to a 4% fully diluted now. I’m very bullish. I’m in on this.

Maurice Jackson: Well, it speaks volumes when you, the CEO, the president, [is] actively buying at current prices. That speaks volumes to the market, and it certainly does for me. I too, am an active buyer myself.

Looking forward, multilayered question: What is the next unanswered question for EMX Royalty? When could we expect a response? And what determines success?

David Cole: So, one of the most frequent questions that I’m [asked] right now is what are you going to do with all the money in the bank? And you’ve seen a recent example—we put $3.5 million to work by buying a 20% interest in the Rawhide gold mine, and we have a plethora of other opportunities that we’re continuing to evaluate.

And we’re focusing on current cashflow, we’re focusing on cash flowing royalties and other cashflow opportunities to enhance our top line, while we’re waiting for things like Timok to come into production and Balya to come into full-scale commercial production, which will occur over the course of the next two years and be transformative to our top line.

And we would like to augment that sooner rather than later with additional purchases of cash-flowing assets. That doesn’t mean that it will for sure happen, but [we] certainly remain alert for opportunities.

One of the main questions I’m asked is, how you can allocate that money? And I can’t say how I’m going to allocate it until it’s done, but our track record is good at allocating capital astutely.

Maurice Jackson: Last question, what did I forget to ask?

David Cole: Well, you’re always pretty good at covering the bases, Maurice. But I can’t think of anything specifically. I will say that we’re just delighted to see some of the traction that we’ve had in the marketplace over the course of the last few months. The stock prices performed nicely. I know I’ve got some new funds that are in there buying the stock that are looking for value situations, and I’m always pleased to see that.

Maurice Jackson: Mr. Cole, if investors want to get more information about EMX Royalty, please share the website address.

David Cole: The website address is www.EMXRoyalty.com.

Maurice Jackson: For direct inquiries, contact Scott Close at (303) 973-8585, or you may e-mail SClose@EMXRoyalty.com. EMX Royalty trades on the TSX.V: EMX | NYSE: EMX. And, just for the record, for the second year in a row, for every Boolean purchase I make this year, I plan on matching in shares in EMX Royalty.

EMX Royalty is a sponsor of Proven and Probable and we are proud shareholders for the virtues conveyed in today’s message. And as a reminder, I’m a licensed representative for Miles Franklin Precious Metals Investments where we provide a number of options to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs and private blockchain-distributed ledger technology. Call me directly at (855) 505-1900,or you may e-mail maurice@milesfranklin.com.

Finally, please subscribe to ProvenAndProbable.com, where we provide mining insights and Boolean sales. David Cole of EMX Royalty, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosure:

1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: EMX Royalty. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: EMX Royalty is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of EMX, Millrock and Newmont Goldcorp, companies mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

( Companies Mentioned: EMX:TSX.V; EMX:NYSE.American,

MRO:TSX.V; MLRKF:OTCQB,

NEM:NYSE,

)